You're Probably Getting Screwed by Credit Cards

And how we can create a healthier financial system

Welcome to You’re Probably Getting Screwed, a weekly newsletter and video series from J.D. Scholten and Justin Stofferahn about the Second Gilded Age and the ways economic concentration is putting politics and profits over working people.

Too Big To Fail Banks are ripping us off. A report issued last week by the Consumer Financial Protection Bureau (CFPB) found the 25 largest credit card issuers are charging customers interest rates that are 8 to 10 percentage points higher than small and medium-sized banks and credit unions. With the average credit card balance being around $5,000 this means $400 to $500 in additional interest - billions of dollars in total - flowing to our Wall Street overlords.

Speaking of those overlords, they saw this damning report as a challenge….to get even larger! Just days after the report’s release Capital One, a bank and credit card issuer, announced plans to acquire Discover, a bank, credit card issuer and credit card network. This $35 billion vertically-integrated mega-merger abomination would create the sixth-largest bank in the United States and the largest credit card issuer by loan volume, further exacerbating the trends the CFPB exposed in its report.

These disparities in rates have a massive impact. Credit card debt has skyrocketed since the financial crisis from around $400 million to over $1 trillion! Meanwhile, in recent years the average interest rate on credit cards has risen to record highs of 22%. Fun fact, loan interest is not included in calculations of the consumer price index (the official measure of inflation) meaning that data showing inflation cooling down doesn’t account for the higher interest people are paying on mortgages, car loans and credit cards.

Some of the CFPB’s significant findings include:

Nine of the largest banks reported having a maximum rate over 30%, including the good folks at Capital One.

Of the large banks analyzed, 27% carried an annual fee, compared to just 9.5% of smaller ones and those fees were generally higher.

Regardless of a consumer’s credit rating, large banks charged higher rates than smaller banks and credit unions.

This is the result of policy choices! For example, while there is an interest rate cap on credit unions of 18%, there is no federal law regulating rates for banks and a 1978 Supreme Court ruling gutted states ability to regulate credit card rates. The attorney arguing in favor of that ruling was none other than Robert Bork, the intellectual leader of the pro-corporate “Chicago School” that helped weaken our antitrust laws and deregulated Wall Street. Fortunately, members of Congress as ideologically diverse as Representative Alexandria Ocasio-Cortez (D - New York) and Senator Josh Hawley (R - Missouri) have introduced legislation that would impose a federal cap on credit card interest rates.

Beyond regulating rates, addressing the extreme consolidation in our banking industry is also critical. Since the 1980s nearly 7 of 10 community banks have disappeared and bank mergers were responsible for 70-75 percent of that loss. As community banks have disappeared it has made it harder for people to accumulate emergency savings, creating greater reliance on things like credit cards and those high rates. This not only impacts consumers, but also entrepreneurs as large banks with their rigid and standardized lending criteria do not lend as much to small businesses as community banks do. This leaves people who don’t have the generational wealth to launch new businesses, like many entrepreneurs of color, more reliant on tools like credit cards to do so.

Stopping bank mergers, like the one between CapitalOne and Discover, is a key piece of this work and having antimonopoly regulators like Assistant Attorney General Jonathan Kanter or a CFPB Director Rohit Chopra (both Biden appointees) is critical, but states can also help. For decades North Dakota’s state bank (The Bank of North Dakota) has helped support a vibrant and distributed banking sector where 83 percent of state deposits are held by smaller banks and credit unions. Short of a state bank, states could replicate The Small Business Banking Initiative in Massachusetts, which has shifted state government bank deposits from Big Banks to local banks and helped spur small business lending.

So call your legislators today! (And for more on the harms of bank consolidation check out this letter from Farm Action and e2 Entrepreneurial Ecosystems.)

YOU’RE PROBABLY (ALSO) GETTING SCREWED BY:

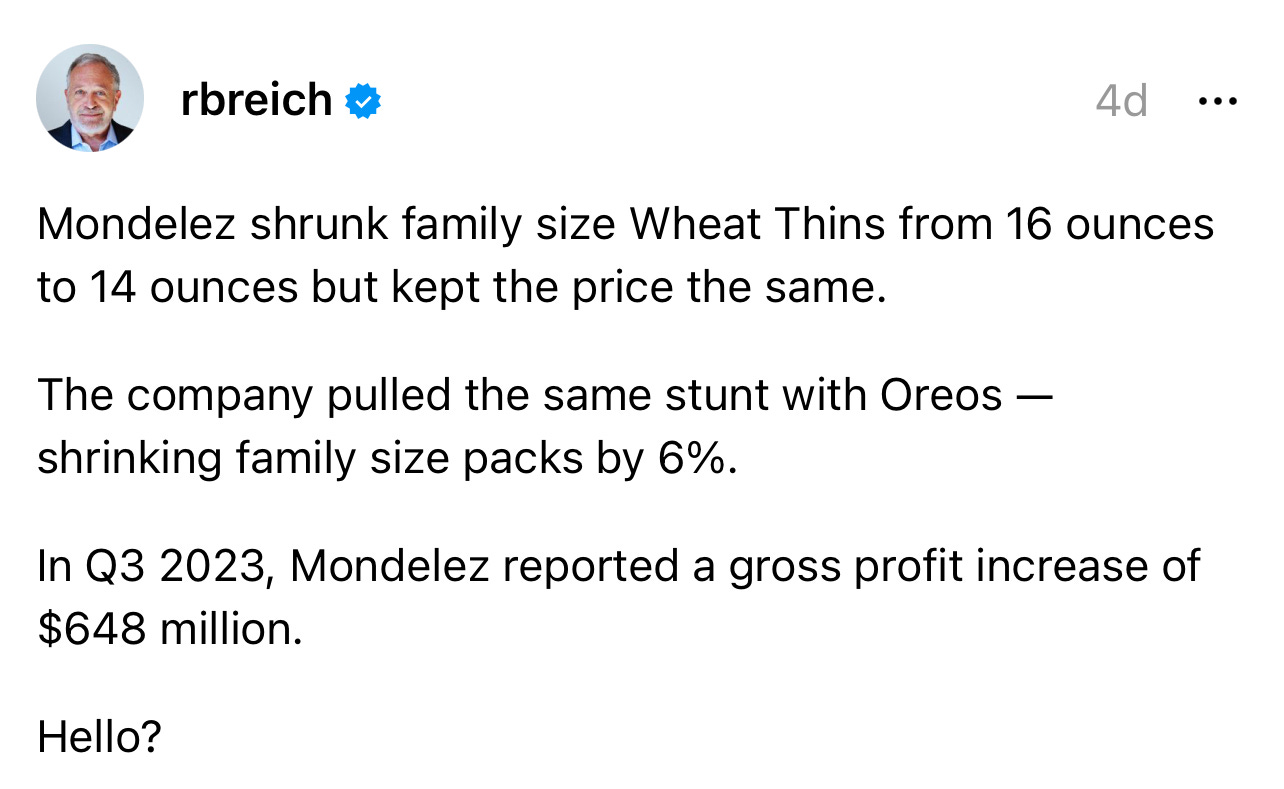

Shrinkflation

Shrinkflation continues!!! Again, here’s what it is, reasons for it, and how to spot it!

Greedflation

Dictionary.com has now defined “Greedflation,” along with “girl dinner” and 1,700 new or updated definitions.

“Greedflation (noun): ‘A rise in prices, rents, or the like, that is not due to market pressure or any other factor organic to the economy, but is caused by corporate executives or boards of directors, property owners, etc., solely to increase profits that are already healthy or excessive.’”

Corporations

The number of American workers hitting the picket lines more than doubled last year as unions flexed. It’s great to see union workers standing up for themselves but these corporations need to step up to the plate. During the pandemic we saw and heard corporations talk about how valuable their employees are, well it’s time to prove it!

Wall Street

This headline: “Did Wall Street kill the American Dream of homeownership? It depends on where you live.”

“You have created a situation where ordinary Americans aren’t bidding against other families, they’re bidding against the billionaires of America for these houses,” Senator Jeff Merkley, who introduced the bill alongside Representative Adam Smith, said, according to the New York Times. “And it’s driving up rents and it’s driving up the home prices.”

More on Capital One Acquiring Discover

Capital One's chances of getting its $35.3 billion deal for Discover Financial past regulators hinge on the bank showing it can disrupt the close-knit U.S. credit card industry, five experts in corporate law interviewed by Reuters said.

Investors are assigning only a 50% chance to the deal being completed amid concerns the proposed acquisition could become a lightning rod for U.S. regulators and lawmakers fretting over high credit card interest rates and fees.

"At the end of the day, the current regime of regulators wants to know if, and how, this merger will benefit consumers," said Abiel Garcia, a former deputy attorney general for the California Department of Justice

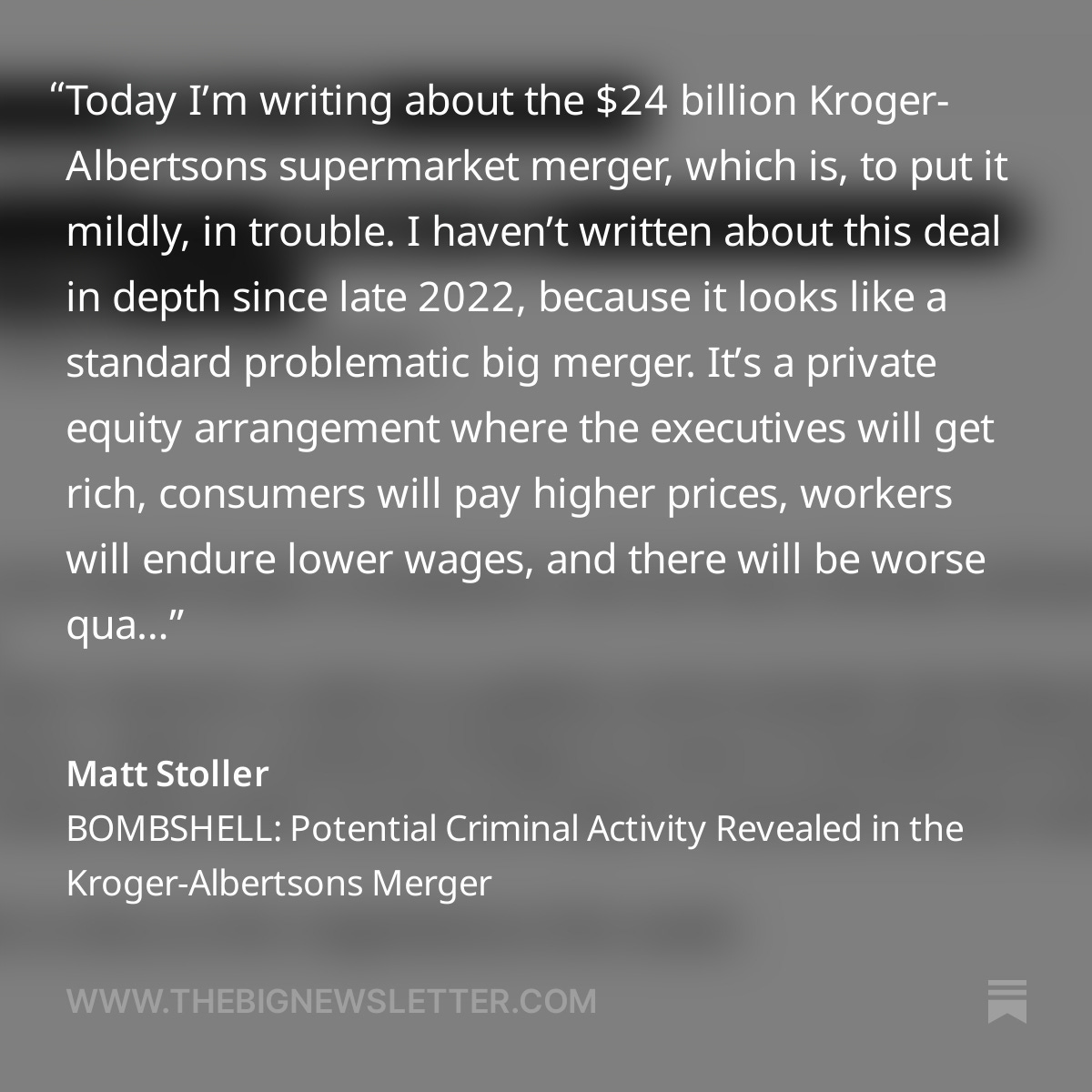

Krogers-Albertsons

Matt Stoller updates us about the Kroger-Albertsons merger. Unshockingly, it will lead to executives getting rich while consumers pay more.

Food Costs

ADVOCACY

BEFORE YOU GO

Before you go, I need two things from you: 1) if you like something, please share it on social media or the next time you have coffee with a friend. 2) Ideas, if you have any ideas for future newsletter content please comment below. Thank you.

Break Em Up!

Justin Stofferahn